Loading...

Loading...

Loading...

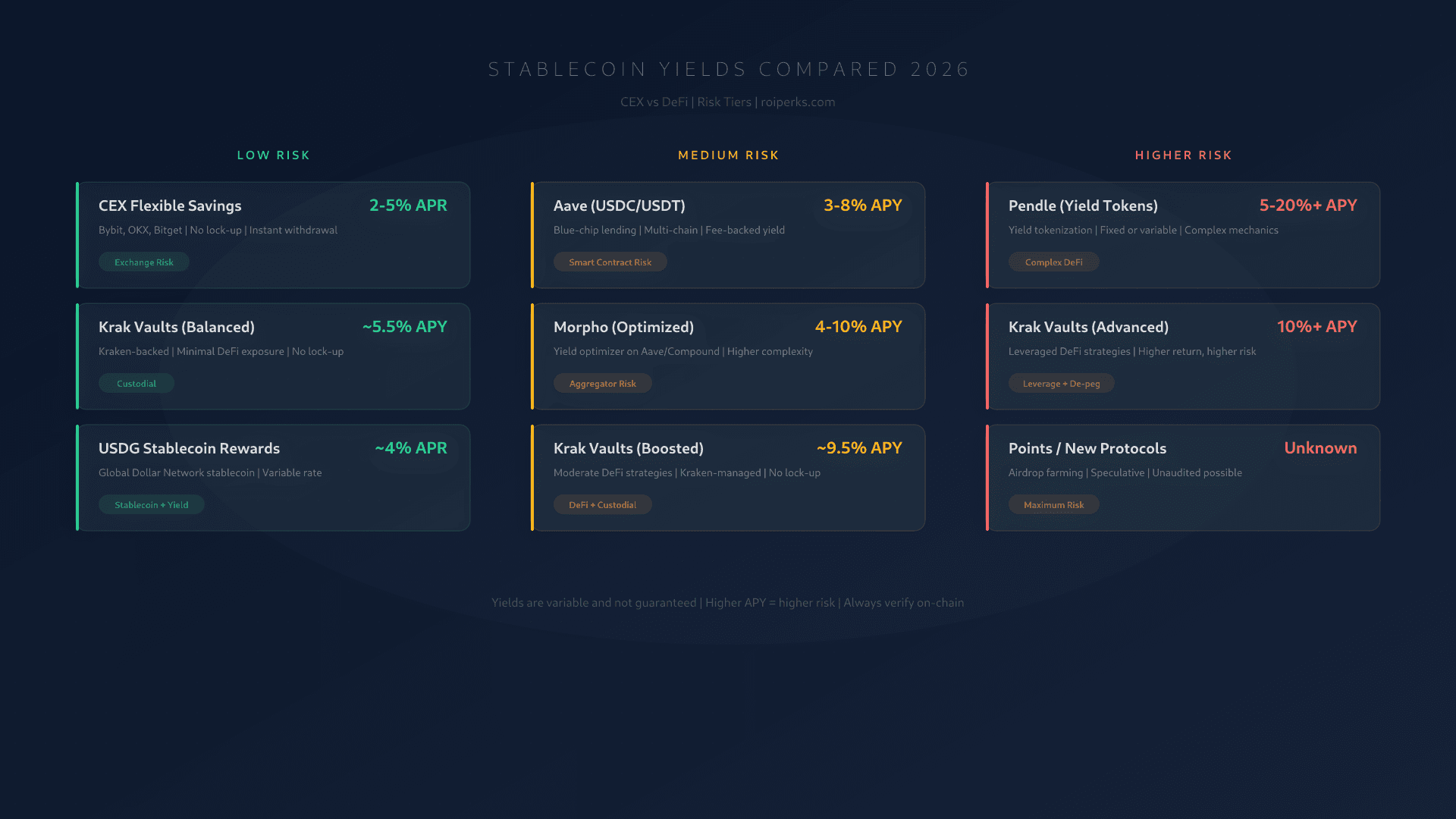

Risk-tiered comparison of stablecoin yield options in 2026. CEX savings, Krak Vaults, Aave, Morpho, Ethena, and Pendle tested and compared on yield, risk, and accessibility.

Holding stablecoins and earning nothing on them is an active choice. Not necessarily a bad one (zero risk has genuine value), but it is a choice worth examining. In 2026, the range of options for putting USDC, USDT, or other stablecoins to work spans from straightforward CEX savings accounts yielding a few percent to DeFi strategies that promise double digits.

The problem is not finding yield. The problem is understanding what you are actually risking to earn it. A platform advertising "up to 15% APY" and one offering "3% flexible savings" are not just different numbers on a spectrum. They represent fundamentally different risk profiles, and the gap between them is where people lose money.

We tested the major options across the risk spectrum: centralized exchange earn products, Krak Vaults, blue-chip DeFi lending protocols, newer yield-splitting mechanisms, and some of the strategies we would actively avoid. This article organizes them by risk tier, because that is the only honest way to compare yields.

Affiliate disclosure: referral links in this article support our testing. We rank on merit and use every product we recommend.

Before comparing specific products, it helps to name the risks clearly. Every stablecoin yield involves at least one of these:

Counterparty risk. Someone else holds your money. If they go insolvent, your deposit is at risk. This applies to every CEX savings product and every custodial yield platform. FTX taught this lesson at industrial scale.

Smart contract risk. Code can have bugs. Even audited protocols have been exploited. The longer a protocol has operated without incident and the more value it secures, the lower (not zero) this risk becomes.

De-peg risk. Stablecoins are stable until they are not. UST's collapse in 2022 wiped out $40 billion. USDC briefly de-pegged to $0.87 during the Silicon Valley Bank crisis in March 2023. Even well-designed stablecoins carry non-zero de-peg risk.

Liquidation risk. Leveraged strategies can be force-closed at a loss if collateral values shift. This is the sharpest risk in the higher tiers and the one most yield advertisements conveniently omit.

Regulatory risk. Yield-bearing products are increasingly attracting regulator attention. What works today may be restricted or restructured tomorrow.

With that framework in place, here is what the yield landscape actually looks like.

These are the options for capital you cannot afford to lose. The yields are modest by crypto standards but beat most traditional savings accounts.

Every major exchange offers some version of this. You deposit USDC or USDT into a savings product, earn interest daily, and can withdraw anytime. Rates across Bybit, OKX, and Bitget hover around 2-5% APR for flexible (instant withdrawal) products. Fixed-term deposits lock your funds for 7 to 90 days and push rates toward 4-8%.

The mechanism varies by exchange. Some lend your stablecoins to margin traders. Others deploy them into money market protocols. The exchange absorbs the operational complexity and passes through a portion of the yield.

The risk is straightforward: you are trusting the exchange not to go bankrupt. After FTX, that is not a formality. Proof of reserves helps but does not eliminate the risk entirely. Splitting deposits across two or three exchanges is a reasonable mitigation.

For most people, this is the right starting point. The yield is not exciting. The simplicity is.

Krak's tiered Vault system starts with the Balanced option, offering up to 5.5% APY with minimal smart contract exposure. Kraken manages the underlying DeFi allocations, so you do not interact with protocols directly. You deposit stablecoins in the Krak app, select the Balanced tier, and earn.

The risk profile sits slightly above pure CEX savings because there is some DeFi protocol exposure underneath, but Kraken's selection of conservative allocations and the company's 14-year track record provide a layer of institutional due diligence that self-directed DeFi does not.

If you are comfortable with Kraken as a custodian but do not want to manage DeFi positions yourself, this is probably the best risk-adjusted option in the lower tier.

USDG is Kraken's own stablecoin, backed 1:1 by fiat reserves. Holding USDG in the Krak app earns approximately 4% APR in base rewards, paid automatically without locking or staking.

The appeal is simplicity: hold the stablecoin, earn yield, no Vault enrollment required. The risk is concentrated in Kraken as both the stablecoin issuer and custodian. If you already trust Kraken as your primary platform, this is low-friction passive income on dormant balances.

This tier involves interacting with DeFi protocols, either directly or through managed products. Smart contract risk becomes the primary concern alongside the counterparty risk that never fully disappears.

Aave is the benchmark for DeFi lending. Deployed on Ethereum, Arbitrum, Optimism, Base, and several other chains, it has processed over $30 billion in cumulative volume and survived multiple market crashes without a protocol-level failure. That track record is not a guarantee of future safety, but it is as close to a proven DeFi protocol as exists in 2026.

Supply rates for USDC and USDT on Aave fluctuate with borrowing demand. During calm markets, expect 3-5% APY. When leverage demand spikes (bull market conditions, major token launches, or macro-driven positioning), rates can push to 7-12% temporarily. You can track real-time rates on the Aave dashboard.

Depositing into Aave requires a self-custody wallet (MetaMask, Rabby, or similar), ETH or the relevant chain's gas token for transaction fees, and basic familiarity with DeFi interfaces. If OKX is your primary exchange, its Web3 wallet can interact with Aave directly without switching apps.

The risk: Aave's smart contracts could contain an undiscovered vulnerability. Four years of operation and billions in TVL make this unlikely but not impossible. Additionally, the stablecoin you supply could de-peg, and borrowers could default in extreme market conditions (Aave's liquidation engine has historically handled this well, but "historically" is not "always").

Morpho sits on top of existing lending protocols (originally Aave and Compound, now with its own Morpho Blue markets) and optimizes rates by matching lenders and borrowers peer-to-peer when possible. Instead of everyone earning the pool rate, matched lenders earn a rate closer to what borrowers pay, eliminating much of the spread the protocol would otherwise capture.

In practice, this means 1-3% higher APY than supplying directly to Aave on the same assets. USDC supply on Morpho-optimized markets typically yields 5-9% APY, occasionally higher during demand spikes.

The additional risk versus raw Aave is the Morpho smart contract layer itself. You are now trusting two protocols instead of one. Morpho has been audited extensively and has operated since 2022 without incident, but the compounded smart contract exposure is real.

For users already comfortable with Aave, Morpho is a logical next step for incremental yield. For DeFi newcomers, start with Aave directly and add Morpho once you understand what you are approving.

The middle tier of Krak's Vault system targets up to 9.5% APY. It achieves this by deploying into a wider range of DeFi protocols with higher utilization and accepting more smart contract exposure than the Balanced tier.

Kraken selects and monitors the underlying protocols, rebalances allocations, and handles the on-chain transactions. For users who want DeFi-level yields without managing wallets, gas fees, and protocol research, Boosted represents managed DeFi exposure with institutional-grade oversight. See our full Krak review for a deeper breakdown of how Vaults work.

The risk is real: the DeFi protocols underlying Boosted could be exploited, and Kraken's management does not eliminate that possibility. The up-to-9.5% headline is a ceiling, not a floor. Actual yields may be lower depending on market conditions and protocol performance.

Ethena's USDe is a synthetic dollar backed by a delta-neutral position: the protocol holds crypto collateral (primarily ETH and BTC) and simultaneously shorts the equivalent value in perpetual futures. The funding rate payments from these short positions generate the yield. Staking USDe into sUSDe passes this yield to holders.

When funding rates are positive (which they are during most market conditions, especially in a bull cycle), sUSDe yields have ranged from 8-15% APY. During bearish or flat markets, rates compress and can occasionally turn negative, though the protocol's reserve fund absorbs short periods of negative funding.

The mechanism is clever but carries meaningful risks. Funding rates could turn persistently negative during a prolonged bear market, exhausting the reserve fund. The custodians holding the collateral (Copper, Ceffu) are single points of failure. And the entire model is, in a sense, a bet that the crypto perpetual futures market continues functioning normally. It has worked well since launch. Whether it works well through every market condition remains an open question.

Ethena is not a beginner product. If you understand how perpetual funding rates work and accept the structural risks, it offers one of the higher yields available on a dollar-denominated asset. If the previous paragraph confused you, stick with Aave.

These strategies offer the highest yields and the highest probability of losing money if you do not understand what you are doing. Capital deployed here should be money you have explicitly decided you can lose.

Pendle is a yield-trading protocol that splits yield-bearing tokens into two components: Principal Tokens (PT) and Yield Tokens (YT). This separation lets you either lock in a fixed yield (by buying PT at a discount to face value) or speculate on variable yield (by buying YT).

The practical application for stablecoin holders: you can supply a yield-bearing stablecoin position (like sUSDe or aUSDC) and sell the yield component for an upfront payment, effectively locking a fixed rate. Or you can buy YT tokens to gain leveraged exposure to future yield, profiting if rates rise above what the market priced in.

Fixed-rate PT positions on major stablecoin pools have yielded 8-15% APY depending on maturity and underlying asset. YT positions are inherently speculative and can generate multiples of the underlying yield or expire worthless.

Pendle's risk is multidimensional: smart contract risk on the Pendle protocol itself, smart contract risk on the underlying yield source, liquidity risk if you need to exit before maturity, and pricing risk on YT positions. The protocol has operated since 2021 and grew significantly through 2024 and 2025. It is well-established by DeFi standards but complex enough that misunderstanding the mechanics can be expensive.

The top tier of Krak Vaults targets 10%+ APY using leveraged DeFi positions. This is not a "higher yield savings account." Leverage means positions can be liquidated if collateral ratios deteriorate. Principal loss is a realistic outcome, not a theoretical footnote.

Kraken manages the execution, which reduces operational risk (you are unlikely to make a fat-finger error on-chain), but the market risk and protocol risk are fully passed through to you. The Advanced tier is appropriate for users who understand leveraged DeFi, accept liquidation risk, and want Kraken to handle the on-chain execution rather than managing it themselves.

Every cycle produces protocols that subsidize early users with token incentives or "points" that convert to governance tokens at a later date. In 2024 and 2025, this included programs from EigenLayer, various liquid restaking protocols, and new lending platforms trying to bootstrap liquidity.

The yields can be extraordinary on paper: 20%, 40%, sometimes higher, when you account for the expected value of future airdrops. The problem is that these yields are speculative, illiquid, and subject to change without notice. A protocol can cut its incentive program, change the conversion ratio, or simply never launch a token.

We include this category for completeness, not as a recommendation. If you understand the specific protocol, have evaluated its smart contract risk independently, and are comfortable with the possibility of earning nothing, selective points farming can supplement a broader yield strategy. As a primary yield source, it is gambling with extra steps.

| Strategy | Typical APY Range | Risk Level | Requires DeFi Wallet? | Key Risk |

|---|---|---|---|---|

| CEX Flexible Savings | 2-5% | Low | No | Exchange insolvency |

| CEX Fixed-Term | 4-8% | Low | No | Exchange insolvency + lock-up |

| Krak Balanced Vault | Up to 5.5% | Low | No | Custodial + light DeFi exposure |

| USDG Base Rewards | ~4% | Low | No | Kraken as issuer + custodian |

| Aave (USDC/USDT) | 3-8% | Medium | Yes | Smart contract + de-peg |

| Morpho | 5-10% | Medium | Yes | Layered smart contract risk |

| Krak Boosted Vault | Up to 9.5% | Medium | No | DeFi protocol exposure |

| Ethena sUSDe | 8-15% | Medium | Yes | Funding rate + custodian risk |

| Pendle PT (fixed) | 8-15% | Higher | Yes | Multi-layer smart contract |

| Pendle YT (variable) | Speculative | High | Yes | Can expire worthless |

| Krak Advanced | 10%+ | Higher | No | Leverage + liquidation |

| Points Farming | Highly variable | High | Yes | Speculative, illiquid, uncertain |

APY ranges are approximate and fluctuate with market conditions. "Up to" figures represent ceilings, not guarantees.

There is no universal answer, but here is a framework that has worked in our testing:

Emergency and operating funds (50-70% of stablecoin holdings). CEX flexible savings or Krak Balanced. Instant withdrawal access, minimal risk. The yield barely covers inflation, and that is fine. The point is liquidity and safety.

Yield-seeking allocation (20-40%). Aave, Morpho, Krak Boosted, or Ethena depending on your risk tolerance and DeFi comfort level. This is where you earn meaningfully more than savings accounts without taking leveraged positions. Diversify across at least two protocols or products.

Speculative yield (0-10%). Pendle fixed-rate positions, Krak Advanced, or selectively farmed points programs. Only with money you have explicitly written off as risk capital. This tier is optional. Many disciplined investors skip it entirely.

The percentages are starting points, not commandments. A trader who manages DeFi positions daily might skew more aggressively. Someone who checks their portfolio quarterly should lean conservative. The important thing is that the allocation reflects a deliberate risk decision, not a vague hope that 15% APY is somehow safe because a slick interface said so.

Spreading stablecoins across multiple venues reduces the impact of any single failure. Keeping everything in one CEX savings account is simple but creates a single point of failure. Consider:

Split CEX savings across two or three exchanges (OKX, Bybit, Bitget all offer competitive rates). Use a separate self-custody wallet for DeFi allocations. Krak Vaults are managed separately from your exchange trading accounts. The operational complexity of maintaining three or four positions is minimal and the risk reduction is meaningful.

Yields above 20% with no clear source. If you cannot identify exactly where the yield comes from (borrower interest, funding rates, protocol subsidies, or token emissions), you are probably the yield. This was the lesson of Anchor Protocol's 20% "stable" rate on UST. The yield was subsidized by token inflation, and when the subsidies ran out, $40 billion evaporated.

Algorithmic stablecoins as yield collateral. After the UST collapse, most investors learned this lesson. Some apparently did not, given the continued launch of under-collateralized algorithmic designs. Stick with fiat-backed stablecoins (USDC, USDT, USDG) or well-collateralized synthetic dollars (Ethena's USDe, with the caveats noted above).

Obscure protocols offering "boosted" rates. A DeFi protocol with $5 million in TVL offering 25% APY on stablecoins is not a hidden gem. It is either subsidizing unsustainably with token emissions or has a vulnerability that has not been exploited yet. Use protocols with at least $100 million in TVL and a multi-year track record.

Locking large positions in illiquid strategies. Fixed-term products and Pendle PT positions have maturity dates. If you need liquidity before maturity, you may face losses on early exit. Never lock more than you can comfortably leave untouched for the full term.

Stablecoin yield is taxable income in most jurisdictions. The exact treatment varies: some countries tax it as interest income, others as capital gains, and some have specific crypto-income categories. Serbia, for example, taxes crypto gains at a flat 15%. Many EU countries treat yield as ordinary income taxed at your marginal rate.

This is not tax advice, and we are not qualified to give it. But ignoring the tax dimension of yield farming is a common mistake. A strategy earning 10% pre-tax that triggers 40% marginal income tax nets 6%. A strategy earning 6% in a jurisdiction with 15% crypto tax nets 5.1%. The difference in actual yield is much smaller than the headline numbers suggest.

Keep records. Every deposit, withdrawal, yield accrual, and protocol interaction is potentially a taxable event. Automated tracking tools (Koinly, CoinTracker, or similar) are not optional if you are active across multiple protocols.

The stablecoin yield market in 2026 is mature enough to offer genuine options across the risk spectrum. You can earn a reasonable return without touching DeFi, or you can extract significantly more yield if you are willing to learn the protocols and accept the risks.

The single most important decision is not which protocol to use. It is how much risk you are actually comfortable taking. Be honest with yourself about that before depositing anything. The difference between 4% and 10% APY feels significant until a smart contract exploit or a funding rate inversion reminds you why the gap exists.

Start simple. CEX savings or Krak Balanced for the core of your holdings. Allocate a smaller portion to medium-risk options once you understand them. Leave the leveraged strategies and speculative farming for genuine risk capital, if you use them at all.

Earn on your stablecoins with our partners: OKX | Bybit | Bitget | Try Krak Vaults for managed DeFi yield

Disclosure: This article contains affiliate links. If you sign up through our links, we may earn a commission at no extra cost to you. This does not influence our assessments. All yield figures are approximate, fluctuate with market conditions, and represent potential returns, not guarantees. This is not financial or tax advice. Always verify current rates and terms on each platform before depositing.

Hands-on review of Krak — the crypto-powered global money app — with instant cross-border transfers, multi-currency wallets, rewards, and referral tips.

Ranked and tested: the seven best crypto exchanges for traders outside the United States in 2026, covering fees, features, security, and real-world availability.

We tested all three. Here is how Bybit, OKX, and Bitget compare on fees, features, security, and what actually matters for non-US traders in 2026.